I posted this article I wrote a few years ago and I thought it needed some updating to reflect how punitive policy has put Canadian housing in peril.

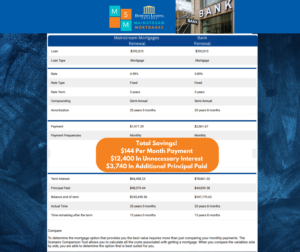

Meet Janet, she is a single mom, earning $55,000 per year, collecting child support of $600 per month, and also collecting CCB of $400 per month. The example of Janet will be used to calculate her maximum purchase price based on each year that the mortgage rules have tightened. Janet has a $20,000 balance on a line of credit.

There are a few things I need to address in this article. I kept property taxes at $3,000 per year consistently through the calculations. Between my memory and what I could find on the internet is what I used for rates. I tried to use a 5 year fixed rate that prevailed throughout the year as much as possible. Is this an exact representation of what Janet could buy? No. Does it give the reader a good understanding of how housing policies affected home ownership, YES!

I think the most disappointing result of these rule changes is that they stunted Canadian real estate development for 16 years. Supply did not keep up with demand. Developers eased their efforts because of fears that no one would be able to buy any properties in their developments. The lack of supply and the lower interest rate environment throughout the pandemic drove housing prices up 20-30%. The pandemic and post-pandemic material prices put construction prices at an all-time high. Today, we have faced one of the fastest and steepest interest rate hikes in history, and this in conjunction with in my opinion terrible policy has put the Real Estate supply in jeopardy for the next decade and beyond. Janet’s purchasing power dropped from $410,000 to a paltry $210,000 over 16 years. The type and size of property she can afford in 2022 are drastically different.

2007

Janet’s Mortgage Maximum: $410,000

Down Payment 0% – $0.00

Rate: 5.70% 5-Year Variable

Amortization 40 years

Monthly Payment: $2,198.02

– No down payment required – finance 100%

– Maximum amortization was 40 years.

– Refinance up to 95% of the value of your home.

– With excellent credit scores of 680+, you could have a Total Debt Service Ratio (TDSR) of 49%

– The minimum credit score for CMHC was 580.

Fall 2008

Janet’s Mortgage Maximum: $425,000

Down Payment 5% – $21,250

Rate: 4.45% 5 Year Variable

Amortization 35 years

Monthly Payment: $1,929.14

– Reduction of maximum amortization from 40 years to 35 years.

– Introduction of a minimum score for Insured mortgages of 620 (But lower scores were

considered on an exception basis).

– 100% financing was eliminated. (However, you could still use a Cash Back Mortgage for

down payment).

-5% Down Payment minimum implemented

– Maximum TDSR lowered to 45%.

Spring 2010

Janet’s Mortgage Maximum: $365,000

Down Payment 5%: $18,250

Rate: 5.85% 5 Year Fixed

Amortization 35 years

Monthly Payment: $1,974.84

– Stricter rental property guidelines. The amount of rent for income/debt servicing

purposes was reduced from 80% to 50%.

– A Mortgage Qualifying Rate was introduced for all insured mortgages on all variable

and fixed-rate mortgage terms 4 years or less. (5-year fixed rate mortgages

were still allowed to qualify at the contract rate).

-The rental Mortgage down payment minimum was raised from 10% to 20%.

– Insured refinances reduced from 95% Loan to Value to 90%.

Spring 2011

Janet’s Mortgage Maximum: $340,000

Down Payment 5%: $17,000

Rate: 5.69% 5 Year Fixed

Amortization 30 years

Monthly Payment: $1909.55

– Insured Home Equity Lines of Credit discontinued.

– Insured refinances further reduced from 90% Loan to value to 85%

– Maximum amortizations lowered further from 35 years to 30 years.

Summer 2012

Janet’s Mortgage Maximum: $305,000

Down Payment 5%: $15,250

Rate: 5.24% 5 Year Fixed

Amortization 25 years

Monthly Payment: $1,777.18

– Implementation of a New Gross Debt Service Ratio maximum of 39%

– Refinance loan to value reduced further from 85% to 80%

– Maximum amortization reduced from 30 years to 25 years for insured mortgages.

OSFI B20 – 2012-2013:

– A new maximum loan-to-value for Home Equity Lines of Credit of 65%, down from 80%.

– The Bank of Canada’s qualifying rate is now applied to all variable and fixed rate

mortgage terms of 4 years or less for conventional mortgages.

– Self-employed borrowers are mandated to provide reasonable income verification. Stated

Income Programs disappear.

– Cashback mortgages are no longer permitted to be used for down payment.

Winter 2014 – OSFI B21

Janet’s Mortgage Maximum: $255,000

Down Payment 5%: $12,750

Rate: 4.79% 5 Year Fixed

Amortization 25 years

Monthly Payment: $1439.54

-Tighter regulations around how to calculate payments on Secured and Home Equity Secured

Lines of Credit.

– All revolving credit payments for debt servicing are now calculated at 3% of the

outstanding balance instead of interest-only payments. For example, a $10,000 credit

card balance would now have a qualifying payment of $300/month up from about $45/month.

Summer 2015

Janet’s Mortgage Maximum: $255,000

Down Payment 5%: $12,750

Rate: 4.64% 5 Year Fixed

Amortization 25 years

Monthly Payment: $1418.25

– Default Mortgage Insurers increase premiums. At a 90.1% – 95% Loan to Value, the premium

increased from 3.15% to 3.6%. This cost to consumers would be an additional $1,350 of

default insurance on a $300,000 mortgage.

2016

Janet’s Mortgage Maximum: $245,000

Down Payment 5%: $12,250

Rate: 4.64% 5 Year Fixed

BoC Qualifying Rate – 5.34%

Amortization 25 years

Monthly Payment: $1,364.93

– Increase the minimum down payments for mortgage amounts between $500,000 and

$999,999.

– Mortgage Insurance is limited to purchase prices not exceeding $999,999

– Insured refinances were eliminated.

– To avoid the abuse of capital gains exemptions, foreign property owners need to prove

that they are selling a primary residence.

– The mortgage stress test expands to 5-year term mortgages but excludes uninsured

conventional mortgages.

2017

Janet’s Mortgage Maximum: $240,000

Down Payment 5%: $12,000

Rate: 4.89% 5 Year Fixed

BoC Qualifying Rate – 5.34%

Amortization 25 years

Monthly Payment: $1,330.91

– Insurers realized revenues are down from all the previous changes and increased premiums.

With a 5% down payment, the mortgage insurance premium jumped from 3.6% to a

WHOPPING 4%. This means that you as a homeowner would have a mere 1% equity interest in

your home.

– It was announced in January 2018 that all conventional mortgages will need to

qualify with their stress test which will be the contract rate of +2.0%. So that means

that if the 5-year fixed rate is 3.49%, you would have to qualify at a rate of 5.49%.

2019

Janet’s Mortgage Maximum: $260,000

Down Payment 5%: $12,750

First Time Home Buyer Incentive 5%: $12,750

Rate: 5.19% 5 Year Fixed

BoC Qualifying Rate: 5.19%

Amortization 25 years

Monthly Payment: $1,429.35

– First Time Homebuyer Incentive is launched.

– RRSP Limit for the Homebuyers Plan increased from $25,000 – $35,000

2020: The Pandemic

Janet’s Mortgage Maximum: $260,000

Down Payment 5%: $12,750

First Time Home Buyer Incentive 5%: $12,750

Rate: 4.79% 5 Year Fixed

BoC Qualifying Rate: 5.19%

Amortization 25 years

Monthly Payment: $1,374.44

-CMHC implements strict lending and underwriting criteria causing it to lose much of its market share.

– Punitive policies included reducing lending ratios increasing credit score minimums to 680, and banning several types of borrowed down payments.

2022: Post Pandemic

Janet’s Mortgage Maximum: $210,000

Down Payment 5%: $10,500

First Time Home Buyer Incentive 5%: $10,500

Rate: 5.99% 5 Year Fixed

BoC Qualifying Rate – 7.99%

Amortization 25 years

Monthly Payment: $1,245.56

Rates started increasing a lot by the end of 2022 posted rates reached a whopping 6.49%

Has the path we have taken to get here been the right one? Probably Not

Were some of these policies a good idea? Absolutely

Did we go too far? Yes!

What needs to change in the industry as a whole?

- Longer amortization for first-time homebuyers

- A review of the stress test. Now that rates have normalized removing the +2% Stress Test is warranted.

- A more common sense approach to underwriting basing the calculations on net income confirmed utility amount per property, and making Gross Debt Service and Total Debt Service ratios more accurate.

- Stability in the residential construction market. The ability/mechanism required to hold a mortgage rate for 1-3 years to allow developers to build condo towers and housing.

- Increase portfolio risk slightly at default mortgage insurers (CMHC, SAGEN, CANADA GUARANTY) our default rate in Canada is less than .05%.

- Better and more accurate credit reporting, or at least the ability to understand credit reporting better. A common sense approach to this is needed.

- Stop the misrepresentation and fraud. There needs to be heftier and more punitive consequences for home buyers, mortgage brokers, REALTORs, Lawyers, Home Inspectors, Banks, and Credit Unions.

- Affordable homeownership programs. Tiny houses, better policy around modular and mobile homes.

- Home renovation programs to help spruce up existing home inventory. I propose having insured refinances available for this sole purpose. Refinance to 90-95% of the value of an existing home to replace windows, roofs, wiring, and mechanical systems, and modernize kitchens, bathrooms, and more.

- The federal government, provinces, and municipalities need to focus on development and home ownership for first-time homebuyers and New Canadians. Land transfer tax exemptions, housing grants, home improvement grants and better permitting processes at all municipal and provincial permitting offices.

If you have an further question we would love to answer them for you!