October 30, 2023

Renting VS. Homeownership:

If you’re a renter in Manitoba and Alberta, you are probably experiencing rental increases at the end of your terms. Many landlords are also being forced out of the market due to higher interest rates or switching to short-term rentals to make more money. This means that many renters will be facing the enormous challenge of having to move and facing unprecedented rental increases in the market.

Depending on your market you will see average rents increasing by double digits. The following information is noted on “rentals.ca” and shows the average rents by city in our main markets as of October 2023.

Winnipeg, Manitoba

1 Bedroom – $1221/month

2 Bedroom – $1636/month

3 Bedroom – $2050/month

Calgary, Alberta

1 Bedroom – $1445/month

2 Bedroom – $1825/month

3 Bedroom – $2655/month

Edmonton, Alberta

1 Bedroom – $1306/month

2 Bedroom – $1618/month

3 Bedroom – $1760/month

One of the most important things to remember is that rental pricing is likely to only increase in the short term. With immigration being at record highs, mortgage qualification rules everchanging, and a high-interest rate environment, make renting a very risky option.

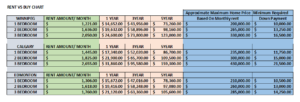

Using the numbers above we have made the following charge. A renter can spend between $73,000 – $160,000 over a 5-year period without building any equity. A homeowner will earn between $21,000 & $45,000 in equity in the same time period and these amounts do not include any increases in property values.

Based on the rental amounts above, these would translate into mortgage payments that could purchase a home priced between $200,000 – $430,000 (please refer to chart)

But, what if you don’t have a down payment?

This can be challenging for many renters and there are a few different strategies to explore:

If you are tired of renting and are looking to get on the path to homeownership, please contact us today!