|

|

|

|

|

Each Office Independently Owned & Operated

Posted by: Peter Paley

|

|

|

|

|

Posted by: Peter Paley

https://globalnews.ca/video/7254618/mortgage-deferral-deadline-looming

Posted by: Peter Paley

MIDTERM MORTGAGE TRANSFERS:

In today’s low interest rate environment, a mid-term mortgage transfer could be an amazing way for you and your family to save thousands of dollars in interest.

Many borrowers don’t think they are able to transfer mid-term, however, it is possible.

To consider this as an options we need to make sure that it is in your best financial interests to pursue it.

When you break your mortgage at your current lender there will be a penalty levied. The new lender will cover all of the fee associated with the switch but not the penalty. The new lender will allow you to include up to $3,000.00 into the new mortgage term. If your current mortgage penalty is greater than $3,000.00 you will need to cover that cost out of pocket.

How much can one save?

Well there are few factors to consider.

I want to offer up an example of a mid-term transfer that we just completed for one of our clients.

Clients had about 38 months left on their existing mortgage term. Their rate was 3.19% with a remaining mortgage balance of $419,438.00. Their current mortgage payments were $2,026 per month. Their penalty was $3,675.00 (Please note that penalty amounts can vary widely depending upon your current lender’s policy).

We prepared the following calculation for them.

We were able to secure them a new mortgage rate of 2.09%. We included $3,000 of their penalty giving them a new mortgage balance of $422,438.00. The new mortgage is going to save them approximately $21,398 just in interest and they will pay an additional $7,000 in principal. Please keep in mind this is on a comparison basis over a new 60 month term. The clients had to pay $675.00 out of their own pockets to make the switch but the financial benefits were substantial.

If you would like to explore your mortgage options and see if a mid-term transfer is right for you, please contact us.

Sincerely,

Peter Paley & Associates

Posted by: Peter Paley

|

– Dr

Posted by: Peter Paley

|

|

|

|

|

Posted by: Peter Paley

Underwriting guidelines are changing again. In many mortgage professionals to the detriment of the economy and recovery. I agree with this analysys.

Please see CMHC’s release below.

The COVID-19 pandemic is affecting all sectors of Canada’s economy, including housing. Job losses, business closures and a drop in immigration are adversely impacting Canada’s housing markets, and CMHC foresees a 9% to 18% decrease in house prices over the next 12 months. In order to protect future home buyers and reduce risk, CMHC is changing its underwriting policies for insured mortgages.

Effective July 1, the following changes will apply for new applications for homeowner transactional and portfolio mortgage insurance:

To further manage the risk to our insurance business, and ultimately taxpayers, during this uncertain time, we have also suspended refinancing for multi-unit mortgage insurance except when the funds are used for repairs or reinvestment in housing. Consultations have begun on the repositioning of our multi-unit mortgage insurance products.

“COVID-19 has exposed long-standing vulnerabilities in our financial markets, and we must act now to protect the economic futures of Canadians,” said Evan Siddall, CMHC’s President and CEO. “These actions will protect home buyers, reduce government and taxpayer risk and support the stability of housing markets while curtailing excessive demand and unsustainable house price growth.”

These decisions are within CMHC’s authorities under the National Housing Act and are in anticipation of potential house price adjustment. We will continue to monitor market conditions and work with our federal colleagues on potential macro-prudential policy options.

CMHC supports the housing market and financial system stability by providing support for Canadians in housing need, and by offering housing research and advice to all levels of Canadian government, consumers and the housing industry.

For more information, follow us on Twitter, YouTube, LinkedIn, Facebook and Instagram.

Leonard Catling

Media Relations

Canada Mortgage and Housing Corporation

604-787-1787

lcatling@cmhc-schl.gc.ca

Posted by: Peter Paley

THE MAINSTREAM MORTGAGE APP – MY MORTGAGE TOOLBOX – Mortgage Comparison Tool

We have the best mortgage app in the country. Our clients and REALTOR partners love it. However, some of you are asking for some tutorials to help with some of its features.

The Compare Side By Side Tool Is a very powerful to help calculate interest savings.

Compare different

– Mortgage Terms

– Interest Rates

– Payment Frequency

– Mortgage Amortizations

– Calculate Interest Savings

– Calculate Extra Princple Paid

– Calculate Payment Savings.

Today’s video will show you how quick and easy it is to compare different mortgage options side-by-side.

Please download our app & enjoy the video. Please share with friends, family and clients!

Posted by: Peter Paley

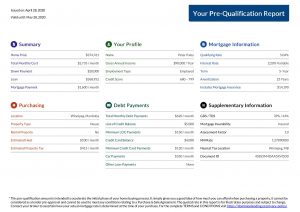

THE MAINSTREAM MORTGAGE APP – MY MORTGAGE TOOLBOX – MORTGAGE PRE-QUALIFICATION TUTORIAL.

We have the best mortgage app in the country. Our clients and REALTOR partners love it. However, some of you are asking for some tutorials to help with some of its features.

You asked and we delivered.

Today’s video tutorial is how to generate a pre-qualification certificate.

Please download our app & enjoy the video. Please share with friends, family and clients!

https://www.youtube.com/watch?v=SAF7eK3sAS4

If you have any clients looking for a mortgage pre-approval or mortgage advice please have them visit our website at www.MainstreamMortgages.Ca or call Peter at 204.227.2744.

Posted by: Peter Paley

As the world pandemic continues, Canada and especially Manitoba are leading in flattening the curve. However, the slowing of the economy has been felt in the number of businesses closed and people filing for employment insurance.

This is leaving many mortgage holders and first time homebuyers in the lurch. Should they defer payments, refinance, sell their home, buy a new home, or continue with their pre-approvals.

The devil is in the details. Every person and family are going to have a very unique set of circumstances and knowing their numbers is the key. Not only do they need to know their numbers, but we need to formulate back up plans as some banks and credit unions are being very cruel when it comes to offering assistance.

As an advisory based mortgage brokerage team we are happy to speak to your clients and see what the best course of action may be for them. Please watch our video below and subscribe to our YouTube Channel.

Posted by: Peter Paley

Over the past month, the Bank of Canada has lowered its overnight rate by a whopping 1.5 percentage points to a mere 0.25%. Many people expected mortgage rates to fall equivalently. The banks have reduced prime rates by the full 150 basis points (bps). But, since the second Bank of Canada rate cut on March 13, banks and other lenders have hiked mortgage rates for fixed- and variable-rate loans. That’s not what happens typically when the Bank cuts its overnight rate. But these are extraordinary times.

The Covid-19 pandemic has disrupted everything, shutting down the entire global economy and damaging business and consumer confidence. No one knows when it will end. This degree of uncertainty and the risk to our health is profoundly unnerving.

Most businesses have ground to a halt, so unemployment has surged. Hourly workers and many of the self-employed have found themselves with no income for an indeterminate period. All but essential workers are staying at home, including vast numbers of students and pre-school children. Nothing like this has happened in the past century. The societal and emotional toll is enormous, and governments at all levels are introducing income support programs for individuals and businesses, but so far, no cheques are in the mail.

In consequence, the economy hasn’t just slowed; it has frozen in place and is rapidly contracting. Travel has stopped. Trade and transport have stopped. Manufacturing and commerce have stopped. And this is happening all over the world.

What’s more, the Saudis and Russians took advantage of the disruption to escalate oil production and drive down prices in a thinly veiled attempt to drive marginal producers in the US and Canada out of business. This has compounded the negative impact on our economy and dramatically intensified the plunge in our stock market.

Many Canadians are now forced to live off their savings or go into debt until employment insurance and other government assistance kicks in, and even when it does, it will not cover 100% of the income loss. The majority of the population has very little savings, so people are resort to drawing on their home equity lines of credit (HELOCs), other credit lines or adding to credit card debt. Businesses are doing the same.

The good news is that people and businesses that already have loans tied to the prime rate are enjoying a significant reduction in their monthly payments. All of the major banks have reduced their prime rates from 3.95% to 2.45%. So people or businesses with floating-rate loans, be they mortgages or HELOCs or commercial lines of credit, have seen their monthly borrowing costs fall by 1.5 percentage points. That helps to reduce the burden of dipping into this source of funds to replace income.

So Why Are Mortgage Rates For New Loans Rising?

These disruptive forces of Covid-19 have markedly reduced the earnings of banks and other lenders and dramatically increased their risk. That is why the stock prices of banks and other publically-traded lenders have fallen very sharply, causing their dividend yields to rise to levels well above government bond yields. As an example, Royal Bank’s stock price has fallen 22% year-to-date (ytd), increasing its annual dividend yield to 5.31%. For CIBC, it has been even worse. Its stock price has fallen 30%, driving its dividend yield to 7.66%. To put this into perspective, the 10-year Government of Canada bond yield is only 0.64%. The gap is a reflection of the investor perception of the risk confronting Canadian banks.

Thus, the cost of funds for banks and other lenders has risen sharply despite the cut in the Bank of Canada’s overnight rate. The cheapest source of funding is short-term deposits–especially savings and chequing accounts. Still, unemployed consumers and shut-down businesses are withdrawing these deposits to pay the rent and put food on the table.

Longer-term deposits called GICs, which stands for Guaranteed Investment Certificates, are a more expensive source of funds. Still, owing to their hefty penalties for early withdrawal, they become a more reliable funding source at a time like this. As noted by Rob Carrick, consumer finance reporter for the Globe and Mail, “GIC rates should be in the toilet right now because that’s what rates broadly do in times of economic stress. But GIC rates follow a similar path to mortgage rates, which have risen lately as lenders price rising default risk into borrowing costs.”

To attract funds, some of the smaller banks have increased their savings and GIC rates. For example, EQ Bank is paying 2.45% on its High-Interest Savings Account and 2.55% on its 5-year GIC. Other small banks are also hiking GIC rates, raising their cost of funds. Rob McLister noted that “The likes of Home Capital, Equitable Bank and Canadian Western Bank have lifted their 1-year GIC rates over 65 bps in the last few weeks, according to data from noted housing analyst Ben Rabidoux.”

The banks are having to set aside funds to cover rising loan loss reserves, which exacerbates their earnings decline. An unusually large component of Canadian bank loan losses is coming from the oil sector. Still, default risk is rising sharply for almost every business, small and large–think airlines, shipping companies, manufacturers, auto dealers, department stores, etc.

Lenders have also been swamped by thousands of applications to defer mortgage payments.

Hence, confronted with rising costs and falling revenues, the banks are tightening their belts. They slashed their prime rates but eliminated the discounts to prime for new variable-rate mortgage loans. Some lenders will no doubt start charging prime plus a premium for such mortgage loans. Banks have also raised fixed-rate mortgage rates as these myriad pressures reducing bank earnings are causing investors to insist banks pay more for the funds they need to remain liquid.

An additional concern is that financial markets have become less and less liquid–sellers cannot find buyers at reasonable prices. The ‘bid-ask’ spreads are widening. That’s why the central bank and CMHC are buying mortgage-backed securities in enormous volumes. That is also why the Bank of Canada has started large-scale weekly buying of government securities and commercial paper. These government entities have become the buyer of last resort, providing liquidity to the mortgage and bond markets.

These markets are crucial to the financial stability of Canada. Large-scale purchases of securities are called “quantitative easing” and have never been used before by the Bank of Canada. It was used extensively by the Fed and other central banks during the 2008-10 financial crisis. When business and consumer confidence is so low that nothing the central bank can do will spur investment and spending, they resort to quantitative easing to keep financial markets functioning. In today’s world, businesses and consumers are locked down, and no one knows when it will end. With so much uncertainty, confidence about the future diminishes. The natural tendency is for people to cancel major expenditures and hunker down.

We are living through an unprecedented period. When the health emergency has passed, we will celebrate a return to a new normal. In the meantime, seemingly odd things will continue to happen in financial markets.